From 6 April 2017, the government is making changes to the way landlords are taxed in the UK. These landlord tax changes will be phased in over the next four years and will not be applied at the full rate straight away – allowing landlords to take necessary action over time.

Here's a resource for those of you wondering, "if I rent my house out do I pay tax?"

Who will the changes affect?

These changes will only affect landlords in the list below who have a mortgage for their rental property.

- Any UK resident individual who lets a residential property in the UK or overseas

- Any non-UK resident individual that lets a residential property in the UK

- An individual who lets residential property in partnership with others

- Trustees of a trust directly holding UK residential property

NOTE: These tax changes will not apply to landlords of furnished holiday lets and commercial properties.

What do the landlord tax changes mean for me?

Restricted tax relief on mortgage interest payments

The main change being made under the new tax rules, is that landlords will no longer be able to fully claim tax relief on their mortgage interest payments – so this change will only affect landlords who have a mortgage and not those who own their property outright.

However, the majority of buy-to-let landlords have an interest-only mortgage.

Currently, landlords can deduct allowable expenses and mortgage interest payments from their rental income and pay tax on the difference.

But from April 2017, landlords will only be able to claim tax relief at the basic rate of 20% on whichever figure is lower:

- Finance costs – including mortgage interest payments, loan repayments, overdrafts

- Profit from your rental income – calculated as rental income less allowable expenses

- Total income – calculated as anything other than savings and dividend income above the personal allowance after deducting losses and tax relief

NOTE: In most circumstances, the finance costs will be the lowest figure. But it’s important to highlight that it’s not just mortgage interest payments that will be used to calculate tax relief, but the lesser of the three figures above.

Here, our infographic helps explain the landlord tax changes:

Click here to embed this infographic in your site

To put this in numbers, if Jane has a rental income of £2,000 per month and her mortgage interest payments are £1,500 a month, under the current rules she will only pay tax – at her current tax rate – on the £500 difference.

However, after all the changes are implemented, Jane will be taxed on her full rental income of £2,000, minus any allowable expenses and can only claim a tax reduction at a maximum of 20%.

Take a look at our landlord tax change examples for a more in-depth break down of what you could be paying after the changes are in full effect.

You may be pushed into a higher tax bracket

If you work, your salary and your rental income will be added together and the rate of tax you pay will be calculated from this value. This could mean that some landlords who are in a lower tax bracket are pushed into a higher tax bracket, as the new rules will increase their total annual income.

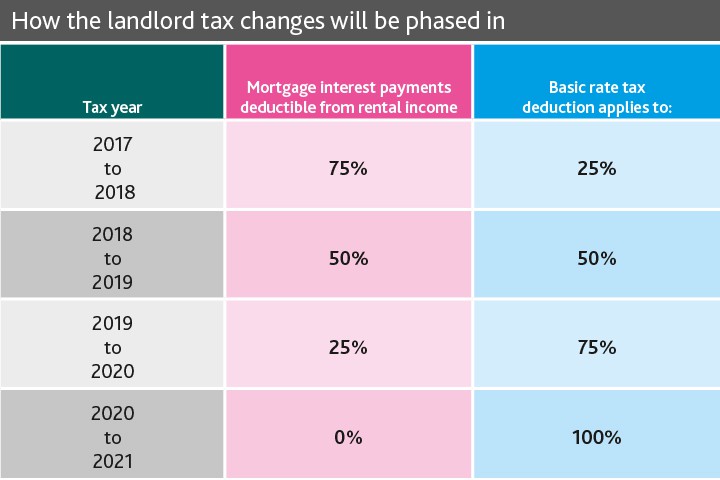

When will the changes happen?

The changes are being phased in from April 2017 to April 2020. Here is an outline of how the changes will be made in stages:

Contact your financial advisor for more information, or questions you may have about the upcoming tax changes for landlords.

*Foxtons have consulted a firm of tax advisers with regards to the content. However, this publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, neither Foxtons, or their tax advisers, accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.